week #22 - 2026

Good afternoon,

We provide a review of the current state of affairs in global macro. Last week we focused on Japan, while this time we take a look at Europe and a bit on the US. Plus, we provide an update on our systematic scorecard.

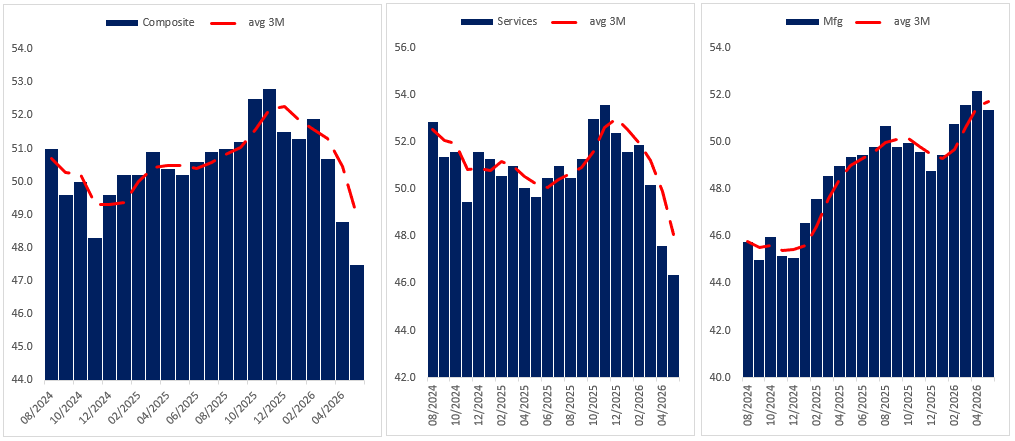

In European markets, I’ve been quite vocal about receiving ECB pricing whenever we approached 3 hikes. This strategy paid off, and by looking at the recent PMIs, we can conclude that the chance of an EZ recession going forward is quite high. First, the EZ PMI slipped to 47.5 from 48.8, the second month in a row below 50, and the trend is clearly deteriorating, driven by services, which printed 46.4. Manufacturing is still holding up (likely due to front-running of orders) and printed 51.4.

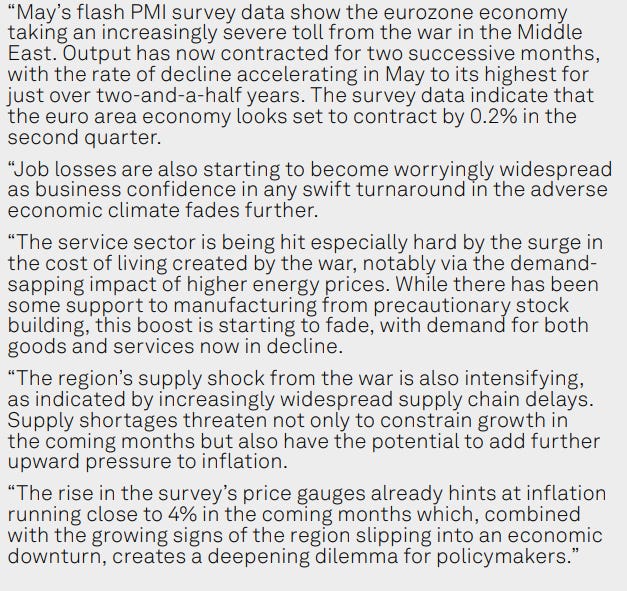

When we look at the comments, it’s pretty clear how cloudy the outlook is:

Inflation is a problem. The ECB will act; it will be a hike, which will worsen the outlook. Pricing is still for 53bp into Z6. We are priced at the top of the range on a 1M basis, so it’s simply better to reduce positioning. Yet, there is more juice to come if we reprice higher in yields again. Probably more flattening on the Z6Z7 section of the curve can be expected.

Keep reading with a 7-day free trial

Subscribe to spaghettilisbon's desk view to keep reading this post and get 7 days of free access to the full post archives.