week #20 - 2026

Global macro update: fiscal, scores and thoughts on euro area.

Good morning folks,

Welcome back to a fresh global macro update. We will cover various topics today and I’m planning to give an extensive review of where we stand on some of the themes I’ve been following.

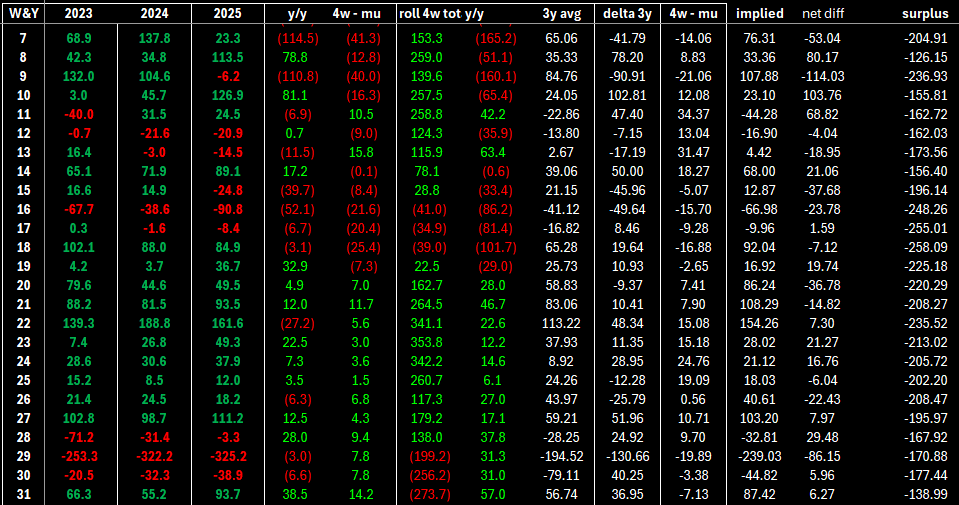

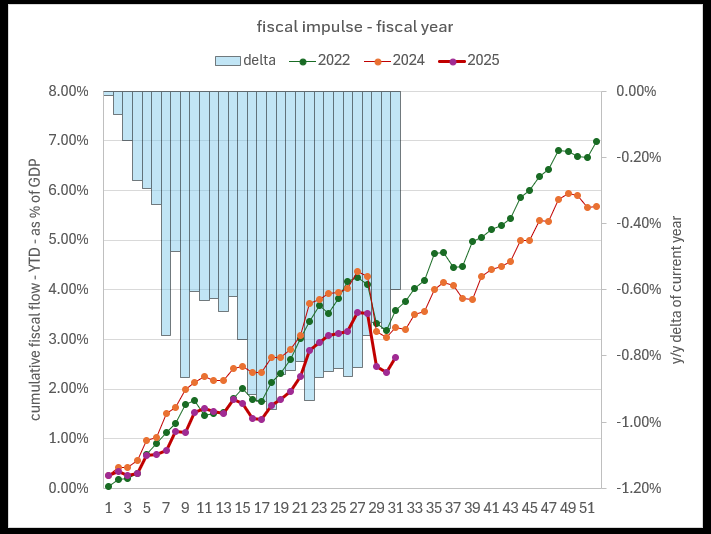

First, a brief recap on fiscal flows. We flagged April, as we do every year, as the draining period for private sector balance sheets. But we also flagged how from thereon flows would ultimately turn bullish, as we would enter one of the strongest periods of fiscal spending of the year. With that said, the overall liquidity drained has been consistent, coming in at roughly USD 367bn, about USD 20bn less than last year.

In the first week after the drain, the private sector balance sheet received USD 97.3bn, and we expect another USD 44bn on average per week over the next five weeks. Still, the impulse remains weak compared to previous years. As of last week, we stand at 2.64% of GDP, well below last year’s value by roughly 60bps, below the 3-year average by 52bps, and below the historical average by 14bps.

While flows have been overall positive, we think this could lead to weakness in the lower income cohort of the population, especially if gasoline prices do not come down in the near future. At that point, fiscal spending would be needed to support the consumer.

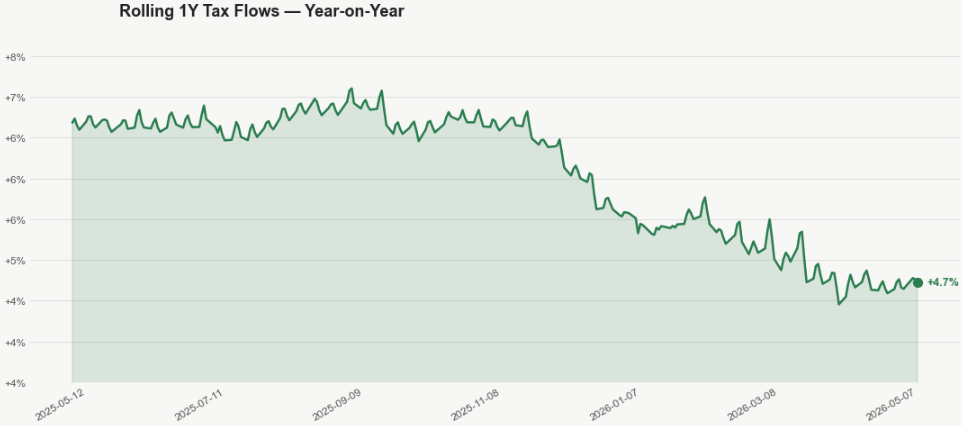

On the consumer side, we track tax flows and continue to see mixed signals. Rolling y/y tax flows are coming down, hovering around 4.7% growth. For now flows have stabilized, but we need to monitor the trend carefully going forward.

With that said, we shift to our scorecard for an equity and rates update.

Starting with rates.

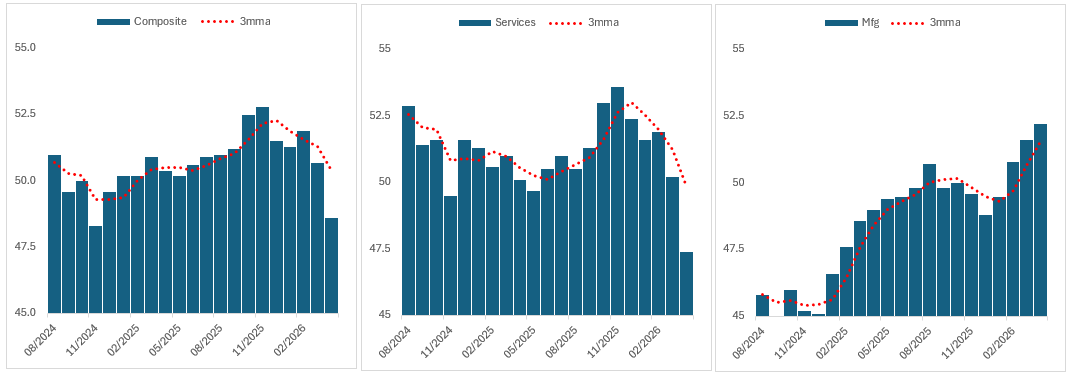

We continue to flag France as a market where to put money to work, though political and budget season is approaching so it’s worth keeping that in mind if you want to run risk. The spread has been tightening over the past few weeks after blowing out during the Iran war risk-off event, and we now sit around 60bps vs. Bunds. We think a lot will be driven by geopolitics, but idiosyncrasies will start to play a role too and may exacerbate moves. Despite the checklist showing France as a good buy and Spain ranking number four, we believe something is not quite adding up in Europe. First, PMI has been rolling over and input prices are skyrocketing, putting pressure on firms.

It takes roughly seven to nine months for these to be passed through to the consumer, but they will show up eventually. The ECB will likely hike in June and then wait to see how things evolve, but I’m biased in thinking they will stay hawkish through this period. I see this as being quite negative for growth. Yes, manufacturing is rising, but it looks like pure front-running, as highlighted in the comments linked here.

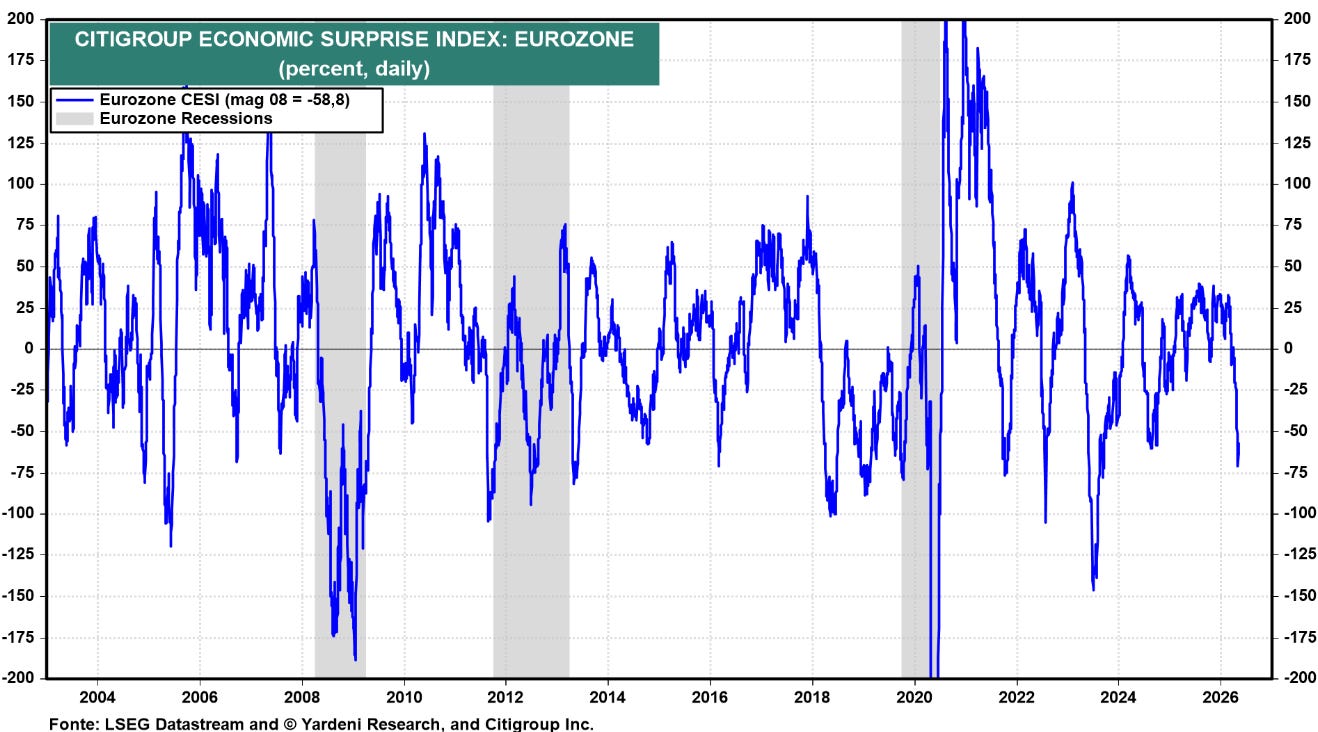

Secondly, we have seen the CESI move sharply lower into negative territory.

On that note, I would also suggest listening to the following interview.

Overall, it’s quite interesting, but the main takeaway is around oil. Everyone seems to think things will normalize and we’ll see oil flowing freely through the strait again, but I’m not so sure about that. It’s not in Iran’s interest to return to the pre-war status quo, and economic pain will show up sooner rather than later — likely by June — making for a difficult summer. Therefore, I’m biased toward staying away from spread tighteners in Europe. I’d actually prefer to play wideners, perhaps in OATs as a tactical trade. There is also room, in my view, to position for more ECB hikes being priced in toward year-end, though this trend will continue only as long as real economic pain hasn’t materialized yet this summer, as I said.

Looking at the rest of the rates dashboard, there is very little to add as most items remained unchanged. JGBs continue to show up on the screen, and we remain skeptical. I’ll be writing a dedicated piece on Japan next week. The UK looks interesting: there’s some political noise going on, and the BoE seems unlikely to pursue further hikes if the slack in the labor market persists. Fading hikes there is probably worth exploring.

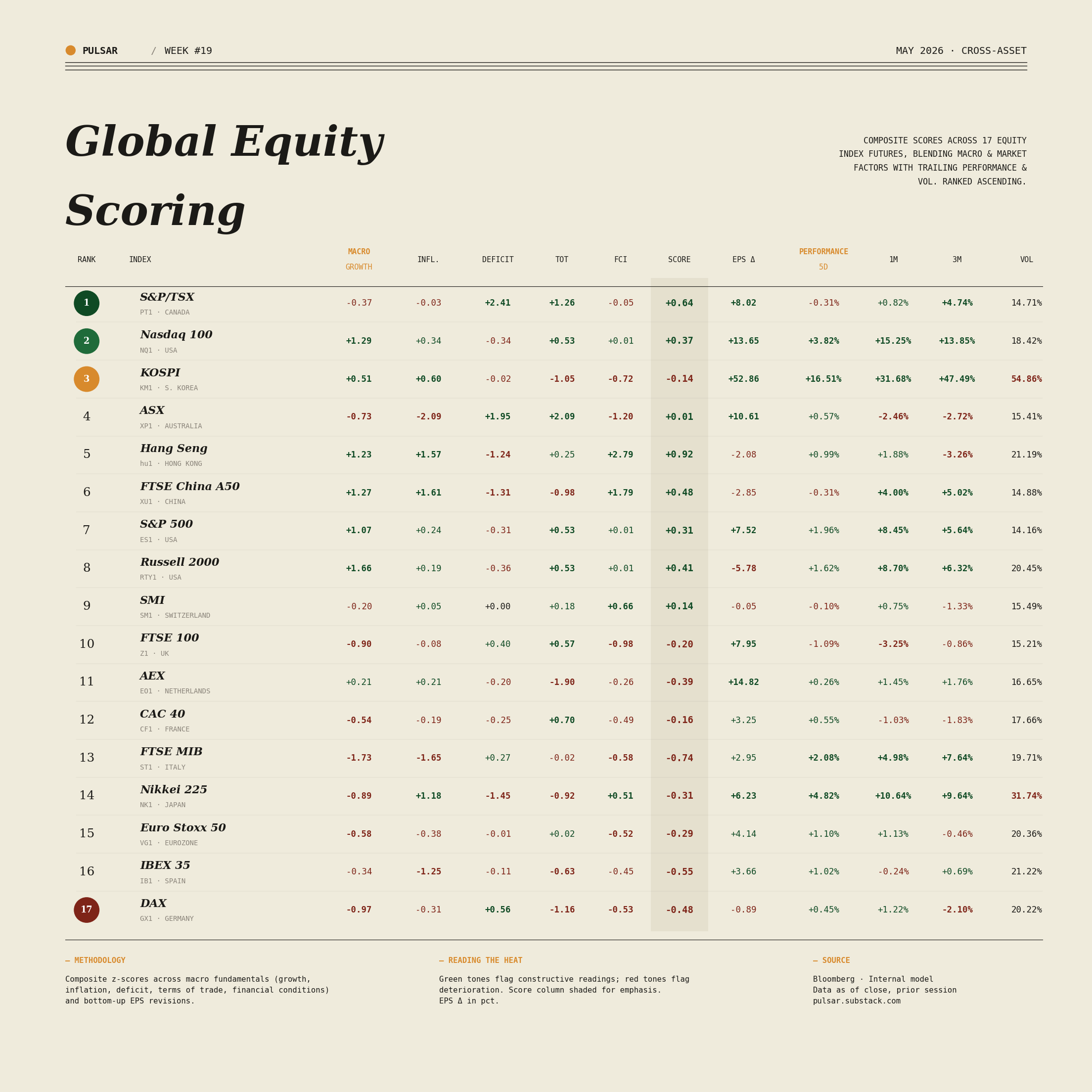

Moving to equities, markets simply don’t seem to care about the war, or they are riding the AI story.

AI-related indices remain our favorite picks, with the Nasdaq and KOSPI ranked second and third, respectively. When we look at EPS revisions in both indices, the numbers are striking — KOSPI is up 52% while the Nasdaq is up 13.6%. On the TSX in Canada, we continue to argue for long TSX versus short Canadian government bonds, which can be expressed cleanly via futures. At the bottom of the rankings, we continue to find European equities.

That’s all for today. Wishing you a great weekend.

Best,

spaghettilisbon