week #10 - 2026

Good evening folks, what a day in markets.

Massive moves in rates, with the US10Y up 9bp and trading above 4% again. The SPX closed green, which speaks to the resilience of US equities and the buy-the-dip mentality that continues to dominate. Either way this plays out, defense spending remains turbo bullish for AI, tech, and defense and we agree with that view.

Europe was the laggard today, but we think a bounce is coming and there is an opportunity to set up the trade we have been running for the past year: the BTP/Bund spread tightener. More on that below. Let’s jump into the scores.

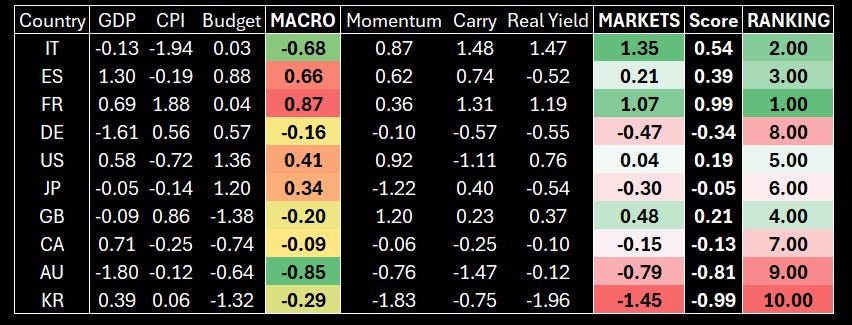

RATES

Very little change in our trading scores. France continues to rank at the top of the list, and with limited headline risk from French politics or budget negotiations, there is scope for longer term tightening.

We also have a positive outlook on Italy and Spain, though for different reasons. Italy looks resilient, particularly from a political standpoint. On the growth side, we are still seeing downward GDP revisions, but composite PMIs are actually pointing to a more constructive picture for Europe broadly. Spain on the other hand has a clear growth advantage relative to the rest of the continent. Overall, we remain constructive on periphery and France, and we continue to think playing these against Bunds, which rank well below them, makes sense. Market signals for Italy and Spain are extremely strong and that is hard to ignore.

Globally, South Korea ranks at the bottom, followed by Australian government bonds. Weak momentum and real yields are the clear drags. JGBs improved in the ranking but we remain structurally bearish given the inflation trend and the BoJ hiking stance. In the UK, we still see scope for outperformance against Germany.

On the US, the economy continues to look sound. Today’s ISM manufacturing print confirmed that, and NFP and CPI could provide further confirmation in the days ahead. We flagged 10Y around 4% as a short and we still like that trade. We think we can run to 4.15/4.20%.

We are also flagging the Germany 2s5s10s fly as extremely attractive right now. It traded as low as 20bp, and adjusting for the level of 5s, we see fair value closer to 14.5bp. We like this trade: if there is further escalation, 5s absorb the volatility, the bar for the ECB to cut remains high, and eventually 10s price in the inflation and growth shock.

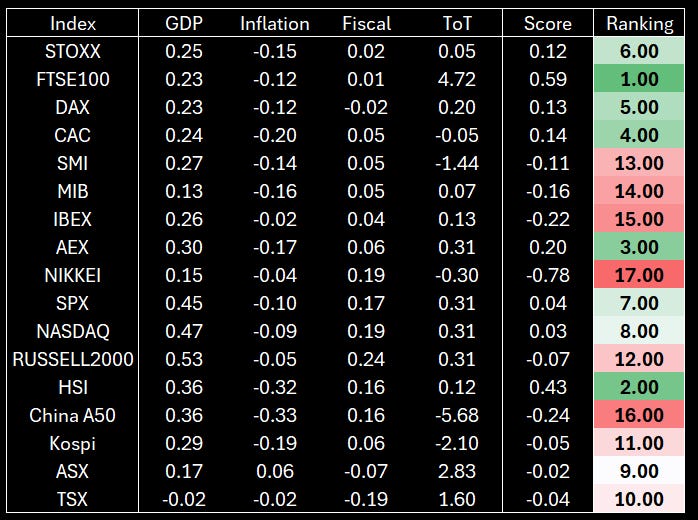

EQUITIES

Quite significant changes in the global macro scoring this week. The FTSE100 remains our top pick, followed by the Hang Seng and the AEX. All three also have positive EPS revisions on a 3 month basis, which supports our allocation.

At the bottom we continue to see some European markets like IBEX and MIB. At the top we have SX5E, SAX and CAC, though only SX5E and IBEX are showing positive EPS revisions, with the others in negative territory. Given that, we do not want to commit too much capital to those positions and prefer to concentrate risk in our core holdings: FTSE100 and Hang Seng.

On the AI trade, we continue to like KOSPI despite the negative macro score. EPS are up 50% so don’t short it.

That’s everything for today. We will be updating fiscal numbers over the next few days.

Have a good evening and stay safe.

spaghettilisbon

When you talk about the 2-5-10 Germany, what do you mean that it is attractive? The current value is -20, if you target -14 it means you want to short the 5y no?

For the RATES table, which Tenor are you using for Real Yield, Carry and Momentum. Are there some weights you use to weigh these before computing their Composite Scores?