Hawkish Pricing, Dovish Reality

Good afternoon folks, it’s time for a global macro update, and we will cover a wide range of markets.

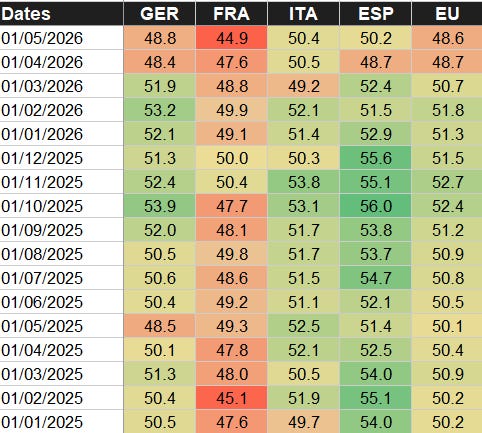

We start by covering Europe, as today we had the full PMIs. As shown below, we printed a 48.5 versus 48.8 the previous month, and by looking at the trend, growth weakness is likely to emerge. Not surprisingly, given the tightening in conditions due to higher oil prices. Prices, as the comment from S&P Global highlights, are running higher and could hit 4%.

The ECB on the 11th is going to hike 25bp, but after that it’s quite hard to say what they are going to do. Looking at the comment from Schnabel, the June hike is a given, but a lot will then depend on price dynamics and the pass-through into the economy. By looking at ECB pricing, we are just below 50bp on the December meeting, going to 50bp in H7. I think this is currently fair and don’t see much value running shorts or longs at the moment. I wouldn’t mind running M7Z7 flatteners if the Iran war continues and, at that point, the rhetoric remains “ECB gonna hike,” as I think growth there will slow down significantly and demand destruction will run its course.

This also leads me to not being that bullish on peripheral spreads. In the current environment, we are seeing BTP-Bund in the low 70s, and I don’t see a catalyst for a much tighter spread. Italian economic performance seems to stay somewhat stable. PMI came in at 50.4 versus 50.5 in April, but, as S&P Global notes, we are seeing services under pressure. I struggle to see meaningful development going forward: the expected GDP forecast has been revised lower, CPI higher, and the budget balance is pretty much unchanged (-3% in 26, -2.8% in 27). But the chants for the government are simply in line with more spending, and it makes sense, as they are trying to defend the economy going into an election year and can’t afford any big setback. I’m keen to be biased toward a widening of the BTP-Bund spread, but it has to be played tactically.

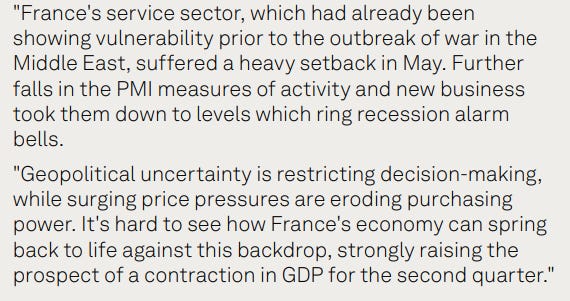

That said, I think a more juicy widening may be against OATs, and it’s easier to play. We have the usual budget discussions coming up, and economic performance is terrible, to say the least. PMI at 44.9, versus a prior 44.9, a 28-month low: “ring recession alarm bells.” Wider we go, I’m saying.

Maybe you can partially fix it with a win at the World Cup but I guess we will probably need a >5% deficit to offset the recession. OATs, yours.

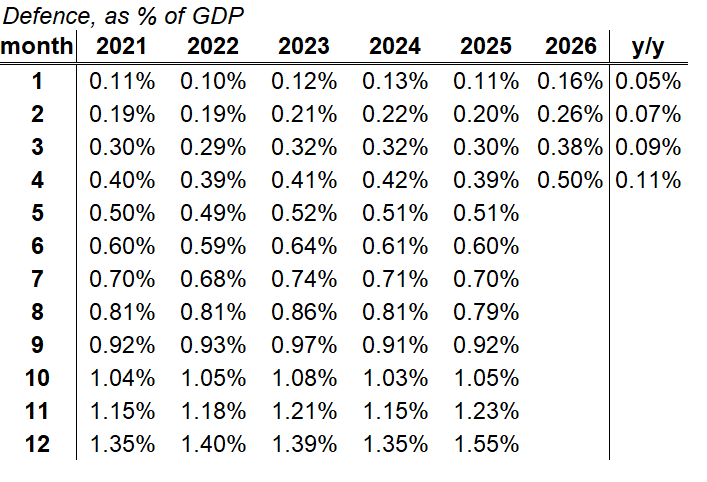

I also want to spend a few words on Germany. There is optimism there; there are inflationary pressures, but they look more stable. By looking at the fiscal impulse, the government is delivering, especially on the defence side. Looking at it GDP-adjusted, we stand at 3.77% as of April, 8bp higher than last year on total spending. In defence, we stand at 50bp of GDP, 11bp above last year. The government is delivering. I keep wondering whether it will be enough to offset the tight conditions driven by higher energy prices, and, to be honest, I don’t have an answer.

Keep reading with a 7-day free trial

Subscribe to spaghettilisbon's desk view to keep reading this post and get 7 days of free access to the full post archives.